StockTalk Restrospective. Bowler Metcalf ltd: the quiet JSE compounder

If you're looking for stability hidden from the public eye on the Johannesburg Stock Exchange (JSE), you'll inevitably stumble upon Bowler Metcalf ltd (JSE: BCF). This company doesn't mine gold, build cloud services, or trade billions of dollars' worth of commodities. It makes plastic bottles, tubes, and caps for your cosmetics, household cleaning products, and yogurts.

Its market capitalization hovers around R1.05 billion - a microcap by JSE standards. But behind this modest façade lies one of the most instructive stories in South African business.

Bowler Metcalf story of success

The company was founded in 1972 in Cape Town, and it has been on the market for 54 years. From day one, the founders instilled a simple rule into Bowler Metcalf's DNA: we don't chase gigantic volumes of cheap, off-the-shelf plastic; we create custom, complex, and high-margin packaging.

If a major shampoo or cream brand needed a unique bottle shape with a complex dispenser, they turned to Bowler Metcalf. The company designed its own molds (for this purpose, they still operate their own tooling facility in Cape Town), in-house blow molded the plastic, and applied the printing.

By the early 2000s, Bowler Metcalf had established itself as a leading player in South Africa's niche rigid plastic packaging industry, operating facilities in Cape Town, Johannesburg, and Durban. The company had already been listed on the Johannesburg Stock Exchange since 1987, but it was during this period that it strengthened its market position and became one of the country's most respected specialist packaging manufacturers

is a classic example of how high-quality, but small and illiquid, stocks perform on the Johannesburg Stock Exchange (JSE).

- All-time low: 250 ZAC (R2.50) – reached on May 21, 2003. This was when the company was just gaining momentum in its experiment with retail beverages.

- All-time high: 2,050 ZAC (R20.50) – reached on August 1, 2024.

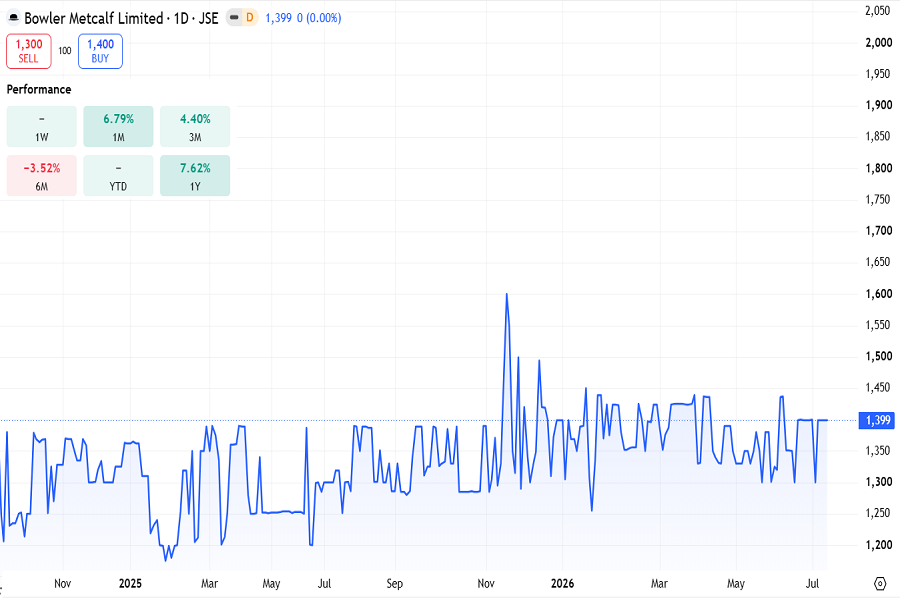

- Current reality: By mid-2026, the price had consolidated and was trading steadily at 1,399 ZAC (R13.99).

Bowler Metcalf's unsuccessful attempts to widen the business

It would seem that if you're so good at making bottles, why not start filling them with your own soda and guarantee sales of plastic? It was this logic that pushed management down a path that nearly cost the company its status as a "dividend aristocrat."

In 2002, Bowler Metcalf acquired a stake in Cape Town-based soft drink producer Quality Beverages (QB) (known for its cult Western Cape brand of cheap soda, Jive, and Vimto). By 2011, Bowler Metcalf had acquired QB entirely for tens of millions of rand.

The business experienced significant growth in its home market of Cape Town. But its ambitions demanded that it conquer all of South Africa. Jive's expansion attempt into the highly competitive Gauteng (Johannesburg) market turned into a financial black hole. Local giants, such as Coca-Cola, waged a price war against the newcomer. Years passed, and the QB beverage division generated millions in losses, eating into the profits of the successful plastics business.

Realizing they had reached a dead end, management decided to retreat: 2015: Bowler Metcalf merges Quality Beverages with competitor Shoreline into a joint venture, SoftBev.

2018 (The Great Exodus): Realizing that retail beverages weren't their game, the board of directors completely sold its stake in SoftBev to The Beverage Company for a hefty R233–R359 million (depending on KPI achievement) plus R79 million in debt repayment.

The sale of SoftBev in 2018 returned Bowler Metcalf to its roots. The company acknowledged its mistake, took profits from the sale, and once again became a pure B2B packaging manufacturer. Shares soared 12% on the news.

This attempt was virtually the only one the company has ever made to grow into a large corporation. What specific miscalculations management made in managing the related business is a question that marketers will have to examine. Did the company have a chance in this market? It did, but intense competition and attempts to engage in price wars without finding its customers proved unsuccessful.

Present Day (2025–2026): BCF as an Investor's Safe Haven

Today, Bowler Metcalf is a compact, highly efficient, debt-free business operating in two segments: Plastic Packaging and Investment Real Estate (leasing its own industrial space).

The company has demonstrated enviable stability while other South African players are struggling with the crisis.

For the second half of 2025 (the six-month report ending December 31, 2025, published in February 2026), revenue increased by 8.2% to R497.3 million, while net profit jumped 16% to R68.5 million. Earnings per share (EPS) for the half-year amounted to R1.00 (versus R0.86 a year earlier).

Shares trade in the range of R13.00 – R14.00 per share. Meanwhile, the forward P/E multiple is at ~7.3x, making the company extremely cheap relative to its earnings growth rate (average EPS growth over the past three years is about 23% per year!).

BCF pays dividends reliably twice a year. The current dividend yield is ~5.2% – 5.4% per annum, and the payout is well covered by free cash flow (payout ratio is about 39%).

Bowler Metcalf stock chart, July 2026

The BCF stock chart shows a stable sideways trend in the range of 1248 - 1454 ZAc. Overall, the stock has hidden potential.

Three components of value: a stable price range, growth prospects, such as through acquisitions or sales of businesses, and dividend payments.

This isn't just a micro-slope. Its distinctive feature is the absence of speculative elements. The stock is still vulnerable to a major purchase or sale, but it's not happening. People buy these stocks not to sell them tomorrow at a higher price, but to receive stable dividends, similar to a bank deposit.

The Future: What Should Investors Expect?

Bowler Metcalf won't be the next rocket that grows 10-fold in a year. It's a classic Value & Income Play.

Management continues to maintain business margins at 13-14%, gradually passing on inflationary costs to customers. The local FMCG market in South Africa is recovering, and Bowler Metcalf is using its cash to acquire one or two more niche plastics companies. Shares are gradually rising to R18.50 (the highs of recent years), providing investors with a stable 5-6% dividend.

Bear Case (Worst Case):

A sharp spike in global polymer prices temporarily compresses profit margins to 9-10%. Shares could correct toward R12.00, but a strong balance sheet and lack of debt will prevent the company from slipping into the red, protecting the dividend flow from being completely eliminated.

Summary

Bowler Metcalf is a quiet, phenomenally effective "dwarf" that has managed to remain profitable and pay dividends for decades. This is a story of how focusing on a narrow niche saves a business, while trying to play on someone else's turf nearly leads to disaster. While this approach may provide the company with immunity from adventurous forays into new markets that risk future stability, it also limits the company's future growth.

The consolidation period we see on the stock chart is neither stagnation nor the calm before the storm. This is BCF's advantage in the stock market. Unlike many companies, Bowler Metcalf shares in an investment portfolio can become the foundation and island of stability that can keep you afloat. Therefore, shares of such companies are probably essential in every investment portfolio.

Stan Lytynsky

Stan Lytynsky is a well known financial expert with more than 1000 of market reviews. For the last 10 years he wrote reviews for different blogs and websites. In particular he worked for SuperForex and Zetradex forex brokers as a market analyst. Currently he is living in Canada and focused on the African market as the most promising and growing.

Related articles

Enjoyed this article?

Get the weekly JSE digest — market recaps, sentiment data, and top analysis, every Sunday.