Altron: 7 basics of success. Special review

Is Altron the Best Buy on the JSE This Year?

Altron showed outstanding financial results in the previous financial period. Investors who bought the company's shares enjoyed impressive growth of nearly 50% in just six months, along with increased dividend payments — and most of them are not planning to sell. Is it worth investing in Altron today, when the price is near its recent peak? Does Altron have real growth prospects? What are the risks of entering the market right now? We explore all of this in our 2026 investment review of Altron.

Investing in Altron can be compared to index trading. The company comprises seven different businesses, each making great financial results, time and again.

The Most Innovative Investment on the JSE

If you've been skeptical of established mining companies, outdated offline retail chains, and other traditional businesses, Altron is the stock you've been looking for. It's hard to imagine a more innovative business in South Africa. This IT company creates software, payment solutions, apps, cutting-edge cybersecurity products, anti-theft systems, and of course AI-powered SaaS solutions.

One Ticker, Seven Growth Points

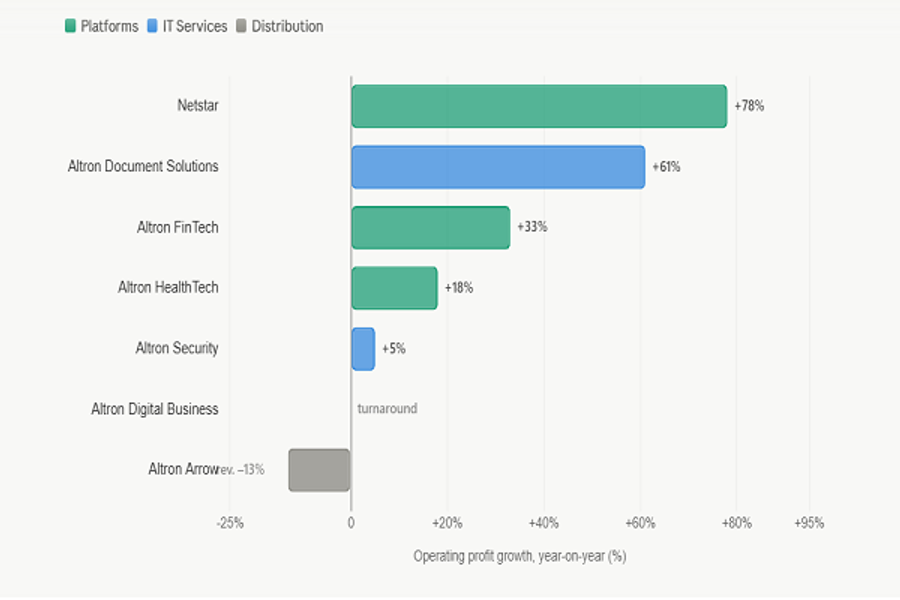

Altron's growth by segments, according to 2026 FY report

Altron operates seven distinct business lines, all of which have demonstrated profitability or a clear path to it in FY2026:

- Netstar — the group's flagship, providing integrated hardware and software solutions for vehicle tracking and fleet management: mobile apps for drivers, GPS tracking equipment, in-car cameras, and cloud-based fleet management software.

- Altron FinTech — payment solutions including the popular NuPay and NuCash systems, debit order processing, POS terminals, and card personalisation.

- Altron HealthTech — innovative, integrated software solutions for healthcare providers, including practice management and medical insurance switching.

- Altron Digital Business — comprehensive IT services for corporate clients: cloud infrastructure, managed services, business optimisation, and digital transformation.

- Altron Security — specialises in cybersecurity, digital identity, PKI infrastructure, and protection of both physical and information assets.

- Altron Document Solutions — the world's largest Xerox distributor and a leading document management technology and services company across 26 countries in sub-Saharan Africa.

- Altron Arrow — a leading distributor of electronic components in sub-Saharan Africa, in a 50/50 joint venture with NYSE-listed Arrow Electronics.

Financial Results and Dividends as Role Models

Published in late May 2026, Altron's FY2026 financial statements are exactly what investors want to see. Operating profits across divisions grew impressively: Netstar surged 78%, Altron Document Solutions rose 61%, and Altron FinTech increased 33%. Group HEPS from continuing operations grew 34% to 239 cents per share, while the three-year CAGR stands at an exceptional 48% per year.

Dividends were equally compelling. The total payout reached R2.40 per share including a special dividend of 120 cents, representing R500 million returned to shareholders. This is a rare signal of management confidence in the company's future cash generation.

Altron faces few serious structural threats. The Altron Arrow division has underperformed in FY2026, with revenue declining 13% due to difficult market conditions in electronic components distribution but this is a cyclical headwind, not a structural failure. Geopolitical risks associated with commodity supply disruptions, which could cause significant damage to energy or manufacturing companies, are largely irrelevant to Altron's software and platform-driven model. This is yet another argument in favour of including Altron in a long-term investment portfolio.

Altron's Fundamental and Technical Recap

Impressed by strong earnings reports and rightly recognising Altron's innovation as well as the broader tech sector's upward trajectory. Analysts are largely constructive on this stock. The consensus view is that Altron not only deserves attention and a place on any watchlist, but that its current valuation remains undervalued relative to its intrinsic worth. The single analyst price target tracked by Investing.com stands at 2860 ZAC, implying upside of over 53% from recent levels. Unum Capital's senior analyst Lester Davids set a momentum target of 3300 ZAC in May 2026. Meanwhile, Simply Wall St's DCF model estimates fair value at R30.67, compared to a current price of approximately R22: a discount of more than 20%.

Altron shares price chart, June 2026

That said, setting aside the strong fundamental signals, a look at the stock chart introduces a note of caution. The price began to decline on the very first trading day of June. Prior to May 25 when the results were published the chart showed a weak, steady upward trend. The company had only returned to growth in November 2025, and all of May's gains were concentrated in just a few candlesticks. This pattern is typically associated with demand overheating around a catalyst event. After such a move, which many experienced traders regard as a non-market price spike, a cooling-off period and price correction tend to follow. Technical analysis indicators currently show a Buy signal across weekly and monthly timeframes but both technical analysis and market intuition suggest it may be worth waiting a few weeks for the price to pull back to a more reasonable entry level before the downward momentum fades.

Results After a Strong Report: When to Buy?

This company's stock has every chance of being the best buy on the JSE this year or at the very least in the second half of 2026. Our long-standing observation that the early months of the year offer the best entry points for quality JSE stocks has once again been confirmed by the Altron chart. In just a few months, the stock soared, and this isn't coincidence - it's a pattern.

If you want your investments to follow a pattern, you should definitely add Altron to your watchlist. The fundamentals are strong, the dividend policy is generous, and the long-term growth story across seven business lines is intact. The only question is timing: with the stock coming off a sharp post-results rally, the most rational approach may be to wait for a consolidation at a non-peak price before entering a position.

Disclaimer: this article is published for informational reasons. Author isn't responsible for consequences of following or not following recommendations if found in the article.

Stan Lytynsky

Stan Lytynsky is a well known financial expert with more than 1000 of market reviews. For the last 10 years he wrote reviews for different blogs and websites. In particular he worked for SuperForex and Zetradex forex brokers as a market analyst. Currently he is living in Canada and focused on the African market as the most promising and growing.

Related articles

Enjoyed this article?

Get the weekly JSE digest — market recaps, sentiment data, and top analysis, every Sunday.